Manufacturing sector set for strong growth and expansion: FICCI Survey

Domestic demand surge, more after GST rate cuts, as 83 per cent of respondents expect higher orders

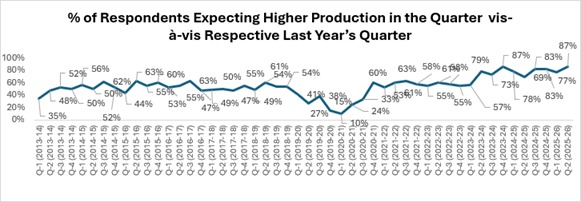

NEW DELHI, India – FICCI’s latest Quarterly Survey on Manufacturing indicates a sustained growth and increasing optimism for India’s manufacturing sector. In comparison to Q1 FY 2025-26, when 77% of respondents reported higher or the same production levels, approximately 87% of respondents reported either higher or the same production levels in Q2 FY 2025-26, according to the FICCI Survey. This is one of the highest percentages witnessed in the last few quarters. This optimism is also evident in domestic demand, as 83% of respondents anticipate an increase in orders in Q2 FY2026 compared to the previous quarter, and even more so after the latest GST rate cuts were announced.

FICCI’s latest Quarterly Survey on Manufacturing (QSM), which is the 67th edition of the survey, assessed the performance and sentiments for Q2 July-September 2025-26 of manufacturers for eight major sectors namely, Automotive & Auto Components, Capital Goods, Chemicals, Fertilizers & Pharmaceuticals, Electronics, White goods & Telecom, Machine Tools, Metal & Metal Products, Textiles, Apparels & Technical Textiles and Miscellaneous.

FICCI’s latest Quarterly Survey on Manufacturing (QSM), which is the 67th edition of the survey, assessed the performance and sentiments for Q2 July-September 2025-26 of manufacturers for eight major sectors namely, Automotive & Auto Components, Capital Goods, Chemicals, Fertilizers & Pharmaceuticals, Electronics, White goods & Telecom, Machine Tools, Metal & Metal Products, Textiles, Apparels & Technical Textiles and Miscellaneous.

Responses have been drawn from manufacturing units from both large and SME segments with a combined annual turnover of over Rs. 3.0 lakh crores.

Capacity Addition & Utilization

- The existing average capacity utilization in manufacturing is close to 75%, which reflects sustained economic activity in the sector.

- The future investment outlook is also positive, with over 50% of respondents indicating plans for investments and expansions in the next six months.

- Challenges faced by respondents in expanding their capacities include global and geopolitical factors (such as tariffs, trade restrictions, and economic uncertainty), operational issues (including labour availability, raw material shortages, and regulatory challenges), and others.

- The table below gives average capacity utilization for various sub-sectors of manufacturing:

Table: Current Average Capacity Utilization levels as reported in the survey (%)

| Sector | Average capacity utilization (%) |

| Automotive & Auto Components | 75 |

| Capital Goods | 70 |

| Chemicals, Fertilisers & Pharmaceuticals | 71.5 |

| Electronics & Electricals | 70.0 |

| Machine Tools | 77 |

| Metal & Metal Products | 75 |

| Miscellaneous | 78 |

| Textiles, Apparel & Technical Textiles | 75 |

| Average | 75 |

Inventories

- In Q1 and Q2 2025-26, more than 90% of the respondents reported a higher or the same level of inventory.

Exports

- In exports, about 61% respondents reported higher or the same level of exports in Q1 FY 2025-26 and in Q2 2025-26, more than 70% of the respondents expect their exports to be higher or the same as compared to the previous year’s similar quarters.

Hiring

- Fifty-seven per cent of the respondents plan to hire an additional workforce within the next three months.

Interest Rate

- The average interest rate paid by the manufacturers has been reported to be 8.9%. A little over 81% of respondents reported having sufficient funds available from banks for working capital or long-term capital.

Sectoral Growth

- Based on expectations, the likely sectoral growth range is shown below:

Table: Growth Expectations for Q-2 FY 2025-26*

| Sector | Growth Expectation |

| Automotive & Auto Components | Strong to Moderate |

| Capital Goods | Strong |

| Chemicals, Fertilizers & Pharmaceuticals | Moderate |

| Electronics & Electricals | Strong |

| Machine Tools | Strong |

| Metal & Metal Products | Strong |

| Miscellaneous | Moderate |

| Textiles, Apparel & Technical Textiles | Moderate |

* Very Strong >20%; Strong 10-20%; Moderate 5-10%; Low < 5%; Source: FICCI Survey

Production Cost

- Production costs for manufacturers in Q1 and Q2 FY 2025-26 seem to remain on higher side. Over 50% of respondents reported an increase in the cost of production as a percentage of sales, which is consistent with the previous quarter’s findings, indicating that costs are still on the higher side.

- The increase in production costs compared to last year is mainly due to higher raw material costs, including key components, bulk chemicals, metallurgical coke, and iron ore, as well as rising labour expenses and increased logistics, power, and utility costs.

Workforce Availability

- Most sectors, though, are not facing a shortage of labour at factories, as less than 80% respondents mentioned that they do not have any issues with workforce availability. The remaining 20% feel that there is still a lack of skilled workforce available in their sector, and there is a need to step up efforts both at the government and Industry level.